.png)

What Is a Disputed Transaction? A 2025 Guide to Chargeback Dispute Resolution

- Alexandre Lebee

- May 20, 2025

- 4 min read

If you've ever seen a transaction on your bank or credit card statement that you didn’t authorize or don’t recognize, your first instinct is probably to dispute it. But what exactly does it mean to dispute a transaction?

In this guide, we’ll clearly define what a disputed transaction is, how it works, when it applies, and how both consumers and businesses can respond. We’ll also explore how AI-powered platforms like AutoDispute.ai are streamlining dispute resolution and helping businesses win more chargebacks in 2025.

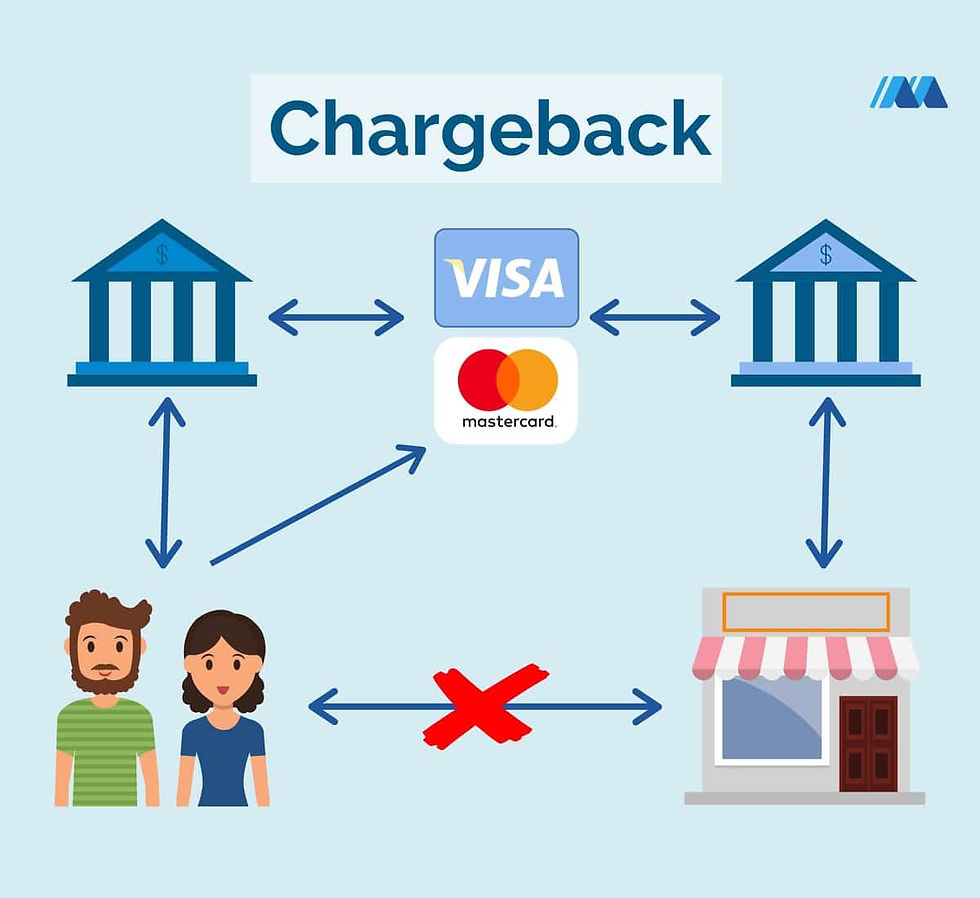

💳 What Is a Disputed Transaction?

A disputed transaction occurs when a cardholder (consumer) challenges a charge on their credit or debit card account, usually because:

The charge was unauthorized or fraudulent

The product or service was never received

There was a billing error or duplicate charge

The merchant violated advertised terms

When a consumer disputes a transaction, their bank or card issuer investigates the claim and may issue a chargeback—a forced reversal of funds from the merchant to the cardholder.

💡 Disputing a transaction is a legal right protected by federal regulations like the EFTA (Electronic Fund Transfer Act) and TILA (Truth in Lending Act).

🧠 Understanding the Dispute Process

Disputed transactions follow a structured path:

Consumer identifies an error on their bank statement.

Dispute is submitted via bank app, phone, or online form.

Issuer contacts the merchant’s bank for investigation.

Merchant responds with documentation (if they contest the dispute).

Decision is made—either refund is granted or denied.

📌 Types of Disputed Transactions

Here are the most common dispute categories:

Dispute Type | Description |

Unauthorized/Fraudulent | Someone else used the card without permission |

Product Not Received | Order was placed but never delivered |

Defective or Misrepresented | Item wasn’t as advertised or arrived broken |

Billing Errors | Duplicate charges or incorrect amounts |

Subscription Cancellation | Billed after service cancellation |

⚖️ Legal Protections: Credit vs. Debit Disputes

Factor | Credit Card | Debit Card |

Governing Law | Truth in Lending Act (TILA) | Electronic Fund Transfer Act (EFTA) |

Dispute Window | 60+ days from statement | 60 days from transaction date |

Fraud Liability | Typically capped at $50 | Capped at $50–$500 depending on timing |

Fund Reversal Timeline | Often faster | Can take up to 45 days |

🔍 Credit card disputes offer stronger consumer protection than debit card disputes. That’s why many experts recommend using credit cards for online purchases.

📞 How to Dispute a Transaction

1. Check the Statement

Make sure the charge isn’t from a legitimate source under a different name.

2. Contact the Merchant

Before escalating to your bank, reach out to the business. Many disputes are resolved without a formal chargeback.

3. Submit the Dispute

Go through your bank’s app or website, or call them. You'll need:

Transaction details (amount, date, merchant)

Description of what went wrong

Supporting documents (emails, screenshots, receipts)

4. Monitor the Case

Your bank may issue a temporary credit while they investigate. Keep an eye out for follow-up requests.

🧾 What Happens If a Merchant Receives a Dispute?

From the merchant’s side, a disputed transaction means revenue is pulled back—often without notice.

Merchants must:

Log in to their payment processor or dispute portal

Review the reason code (e.g., 13.2 – Canceled Recurring Transaction)

Submit compelling evidence within a set timeframe (usually 7–10 days)

🧠 The response must match the dispute reason. Submitting mismatched or irrelevant documentation is one of the biggest reasons businesses lose chargebacks.

🤖 Why AI Is Essential for Dispute Management in 2025

Dispute resolution is complex. Each card network (Visa, Mastercard, AmEx, etc.) has different rules. And volumes are rising—especially with ecommerce growth and fraud upticks.

That’s where AutoDispute.ai comes in.

AutoDispute helps businesses:

Get notified instantly when a dispute is filed

Auto-generate representments (response packets) using transaction data

Attach compliant evidence based on reason code

Track dispute success rates and identify risk trends

📈 Merchants using AI platforms like AutoDispute see 30–50% higher win rates, reduced manual work, and lower payment risk overall.

📉 What Happens If You Lose the Dispute?

If You’re a Consumer:

The bank may deny your claim and re-debit your account

You can appeal the case or escalate to the CFPB (Consumer Financial Protection Bureau)

If You’re a Merchant:

You lose the disputed amount plus a chargeback fee

Too many disputes may lead to account holds, higher processing fees, or blacklisting

🔐 How to Avoid Disputed Transactions

For Consumers:

Use credit cards instead of debit cards online

Opt for 2FA and fraud alerts from your bank

Save receipts and shipping confirmations

For Merchants:

Use clear product descriptions and refund policies

Enable real-time fraud protection tools

Leverage AI to automate chargeback defense

🎯 Pro tip: AutoDispute.ai offers end-to-end automation for dispute response and recovery.

🔄 Real-Life Example

Case: Jake vs. Duplicate Streaming Subscription

Jake was charged twice for the same streaming plan. He disputed the second charge with his bank, submitting screenshots of his account page and receipts. The bank issued a provisional credit, and the merchant confirmed the error.

✅ Result: Dispute approved, refund processed in 4 days.

Now imagine that merchant didn't respond in time—or didn’t attach the correct documents. That’s revenue lost.

🧩 Frequently Asked Questions

What does “disputed transaction” mean on my bank statement?

It means you (or someone with access to your account) have challenged a charge, and your bank is currently investigating.

How long does it take to resolve a dispute?

Anywhere from 5 to 45 days, depending on the bank, card network, and complexity of the claim.

Can merchants fight back?

Yes. If the merchant provides valid evidence and the charge is proven to be legitimate, the dispute may be denied.

🛠️ How AutoDispute Helps You Win

Whether you're managing 10 disputes a month or 10,000, manual dispute handling just doesn't scale.

That’s why AutoDispute.ai is the platform of choice for modern businesses.

Key Features:

AI-powered evidence generation

Real-time alerts + integrations

Transparent analytics on win/loss rates

Full support for Visa, Mastercard, AmEx, and more

📊 Stop reacting. Start defending—and winning.

🎯 Final Thoughts: Know Your Rights. Use the Right Tools.

A disputed transaction doesn’t have to be a crisis. Whether you’re a consumer safeguarding your funds or a merchant defending against chargebacks, knowing what to do—and acting fast—is key.

But to win consistently, especially at scale, you need more than just policy. You need precision.

👉 Ready to Win More Disputes?

If you're serious about reclaiming revenue and reducing operational drag:

Let AI handle the disputes—so you can get back to growing your business.

Comments